Goals Based Investing

We believe investing is about selecting quality investments to build a custom portfolio that is designed to provide the income and stability you need to maintain the type of lifestyle to which you have become accustomed and to help you reach the goals you have for your future.

Managing Risk

Based upon your priorities and tolerance for risk, your personalized eMoney® plan will seek to avoid unnecessary investment risk. It is designed to provide a sophisticated roadmap to help you reach your financial goals.

Core – Satellite Portfolio Construction1

We employ the basic principle of non-correlating asset classes as we develop your portfolio. The CORE portfolio makes up the majority of the investment assets and it is customized to the unique needs of each particular client. We then add in a SATELLITE strategy of non-traditional, or alternative, asset classes as appropriate. This CORE/SATELLITE strategy seeks to give you traditional market exposure for while adding the additional diversification of alternative asset classes that can drag performance in good years but can add significant stability in bad years. Managed futures, hedge funds, private equity and real estate investment trusts can offer our clients an added level of sophistication and diversification.

Tax-Efficient Investment Strategies

The long-term impact of taxes on investment returns can take a bite out of your savings. Our tax-efficient strategies help you continue to grow your savings for retirement while striving to address the impact of taxes.

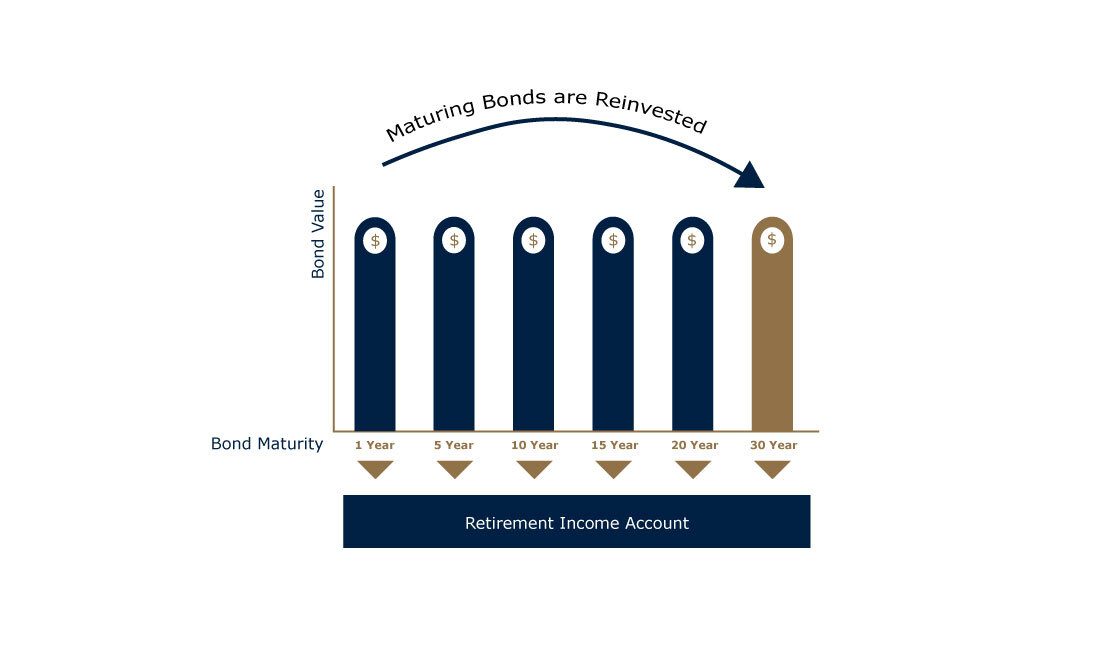

Bond Laddering to Create Your Monthly Retirement Income2

To create your stream of monthly potential retirement income, we employ a bond laddering strategy to spread investment dollars among bonds that mature at various times between one year and 30 years. To create your portfolio of laddered bonds we purchase bonds of staggered maturities to offset fluctuating interest rates, increase portfolio diversification, and fulfill your specific income requirements.

To help visualize the portfolio think of individual bonds as rungs on a ladder. In normal interest-rate environments, bonds with shorter maturities will yield less than longer maturities. As each individual bond in the ladder matures (bottom rung), the principal then becomes available for reinvesting, at current interest rates, into bonds of intermediate or longer-term maturities with the higher yields. The new bonds then become the new “top rungs” of the ladder.

Adding Value

Our team is dedicated to helping ensure that your needs are always our priority. With a deep focus on you, your family and your next generation, we work to have meaningful conversations and listen carefully, so you’ll know you have an investment plan in place to help pursue your life’s priorities and passions.

1 Wells Fargo Advisors are not a legal or tax advisor. Advisory services are not designed for excessively traded or inactive accounts and is not appropriate for all investors. There is a minimum fee per calendar quarter to maintain this type of account. During periods of lower trading activity, your costs might be lower if a clients' account was based upon commissions. Please carefully review the Wells Fargo advisory disclosure document for a full description of our services. The minimum account size for these programs is $25,000 to $200,000. Insurance products are offered through nonbank insurance agency affiliates of Wells Fargo & Company and are underwritten by unaffiliated insurance companies. Any estate plan should be reviewed by an attorney who specializes in estate planning and is licensed to practice law in your state.

2 Alternative investments are not appropriate for all investors and are only open to “accredited” or “qualified” investors within the meaning of the U.S. securities laws. They are speculative, highly illiquid, and are designed for long-term investment, and not as trading vehicles. They are intended for qualified, financially sophisticated investors who can bear the risks associated with these investments

3 Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income investments may be worth less than original cost upon redemption or maturity. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. Bond laddering does not assure a profit or protect against loss in a declining market. Yields and market values will fluctuate, and if sold prior to maturity, bonds may be worth more or less than the original investment. All investing involves risk, including the possible loss of principal.